It has been a while since I have started this blog. It has been enriching being more disciplined in creating original content (while curating some). Looking back over these 49 blog post entries, I thought it might be a good time to take a pause – and collate in the 50th entry some of the original content I created in the process. So here it follows …

“PayPal has unveiled the launch of PayPal Beacon, a plug-in device for merchants that is set to enable consumers to make hands-free payments in a number of stores.

PayPal Beacon is set to leverage Bluetooth Low Energy, a technology that enables connected devices to communicate with each other, while keeping the energy consumption at a low level. By using BLE, transactions can take place with no app being opened, without GPS being turned on and without a phone signal..”

In an attempt to better understand and apply the blue-ocean strategy, I decided to test the framework on a rapidly evolving market – the payment’s industry.

The solutions in the payments industry can be broadly classified into categories: those addressing emerging economies and those addressing developed economies. It naturally follows that the value propositions of the payments solutions in these two segments are quite apart and hence the associated value networks differ as well.

Here, I take a look at the developed economy market and specifically into a trend that has attracted several firms – mobile point of sale (mPOS).

In its simplest form, mPOS can be described as a payment-terminal (like the traditional credit card terminal) on your phone! Well it literally is that – pay using a mobile device (Smartphone/Tablet) and use funds from the traditional card accounts (magnetic stripe cards and the chip & pin EMV cards). Vendors like SumUp and Square Inc. are good examples.

The surge of companies in this space indicate a rapidly evolving technology area wherein there is yet to be a dominant technology. But it has seen innovative business models and new value propositions.

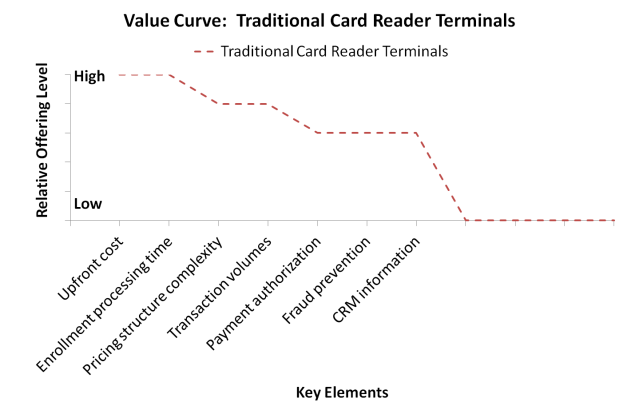

The key elements of the traditional credit card terminal used at retail outlets have the following characteristics:

Key elements

Value to customer

Upfront cost

A significant fixed cost is involved to procure such a device (Anything between $150 to $1000 per terminal depending on product specifications)

Enrollment processing time

This involves enrolling with payment solution providers and fulfilling a barrage of legal requirements to get the process started.

Pricing structure complexity

In addition to an initial fixed cost, there are monthly maintenance charges that could be accompanied with long term agreement charges and other complex pricing structure.

Transaction volumes

The high fixed cost and complex pricing structure necessitate a certain number of transactions to break even.

Payment authorization

End users that swipe their cards through these terminals feel secure due to pin-entry provision.

Fraud prevention

It follows that both front-end and back-end systems must complement to avoid fraudster from abusing the payment systems.

CRM information

CRM software and other middleware solutions can enable merchants to pull out relevant sales information transacted through the payment terminal

The value curve for the traditional credit-card terminal industry would look as below:

Traditional Credit Card Terminals – Key Elements and its relative offering level

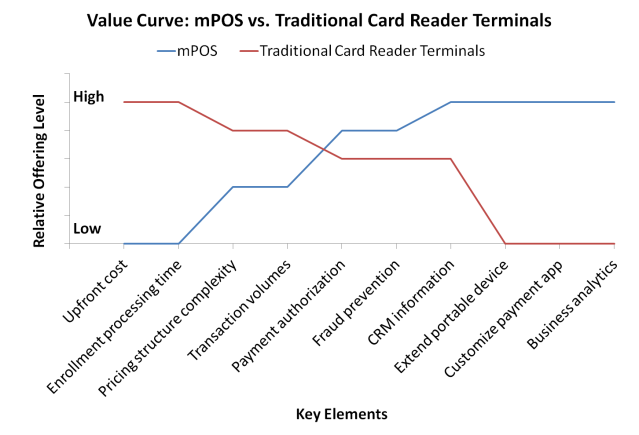

Vendors likes SumUp and Square Inc. have however reversed this curve, and brought to the fore the mPOS dongle that extends the ubiquitous Smartphone (& tablet) into a payment terminal. Taking advantage of the app-store eco-system it provides merchants with a basic application for usage and also allows merchants to create customized apps to exploit the backend services. Merchants can take this a step ahead to analyze the sales data & customer preferences and thus derive business intelligence. All this comes at zero additional charges – the dongle comes for free – and in short turnaround time.

The grid below indicates the application of the Four-Action Framework (ERRC) – depicting a change in priorities of the key elements identified before, in addition to additional elements provided by the new offering.

Four Action Grid – mPOS

Eliminating the high fixed investment and cutting down the enrolment process drastically, these vendors have been able to attract a new customer segment – micro-merchants – those that traditionally stayed away from the card-terminal and primarily dealt in cash.

mPOS vendors maintain a simple revenue model – charging a fixed percentage of sales revenue (typically 2.75% as of today). mPOS thus met the unmet need of a previously ignored segment of customer. An analogy I can think of here is text-based mobile banking (like M-PESA) in emerging economies – it met the banking needs of the un-banked customers in such geographies.

The value curve of the mPOS solution is overlay-ed on the previous chart as shown below:

mPOS vs. Traditonal Payment Terminal value curve

Clearly mPOS is an interesting proposition for the payments industry. While the use of this ‘cool’ gadget may sync with the brand image of some merchants, there is need for caution. mPOS vendors must seek to address concerns, if any, of consumers reluctant to type in their PINS into a merchant’s phone or tablet!